The East Bay/Oakland industrial market demonstrated remarkable resilience in Q2 2025, navigating economic headwinds and evolving tenant priorities with steady fundamentals and strategic repositioning.

Market Trends Snapshot

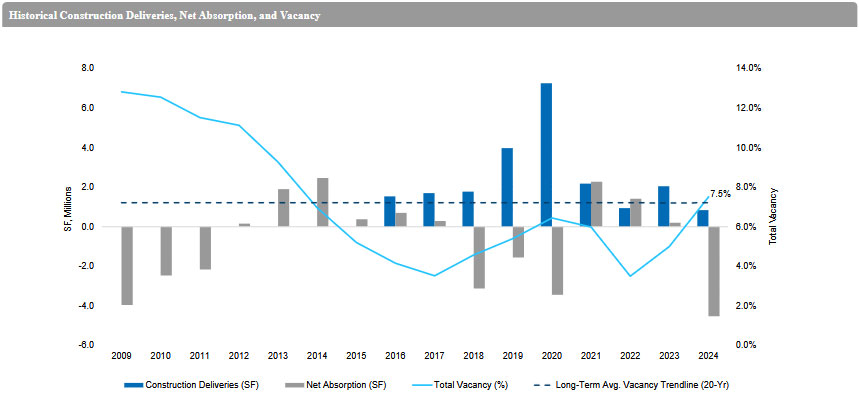

- The East Bay/Oakland industrial market saw a notable shift in Q2 2025, with the vacancy rate climbing to 9.2%, up from 6.5% a year ago. This marks the sixth consecutive quarter of negative net absorption, underscoring a period of sustained occupancy losses as tenants recalibrate their space needs.

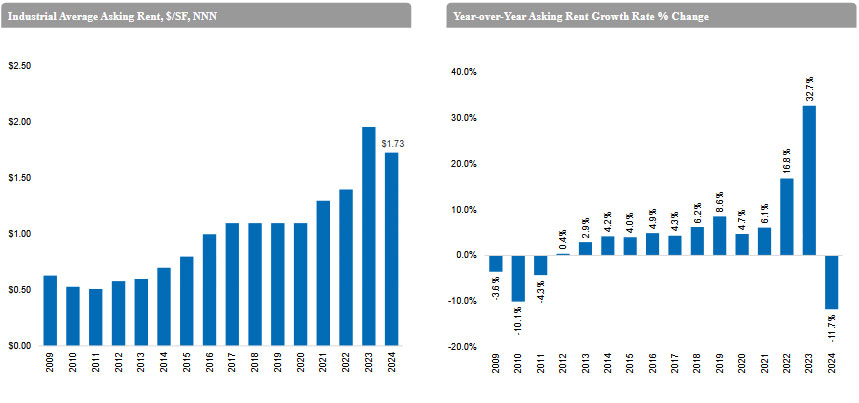

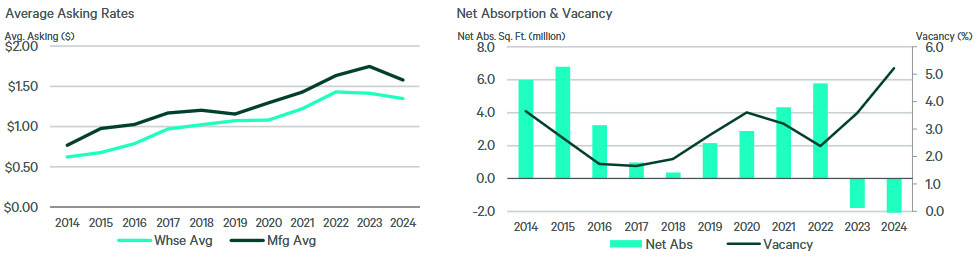

- Despite the elevated vacancy, asking rents remained resilient at $1.30 per square foot, dipping just 1.4% from Q1 but still up 15.6% year-over-year, reflecting the region’s long-term value proposition.

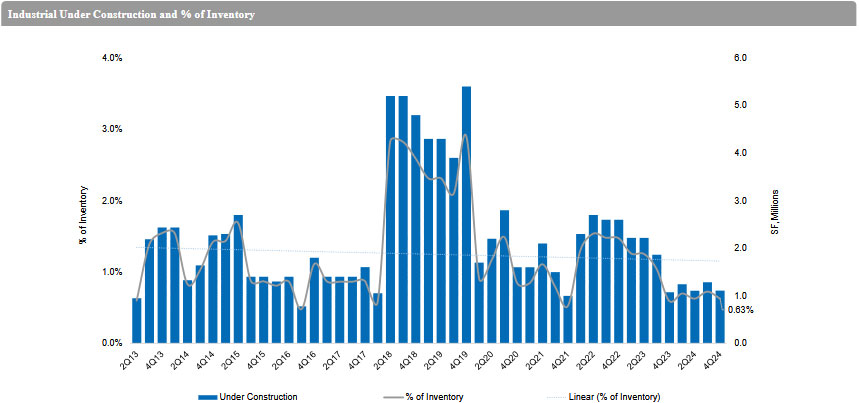

- On the development front, construction activity has slowed significantly. Less than 100,000 square feet of new space is currently underway—down sharply from 835,203 square feet last quarter. However, the market welcomed 1.3 million square feet of completed deliveries so far this year, adding fresh inventory to meet evolving tenant demand.

Leasing Activity & Tenant Trends

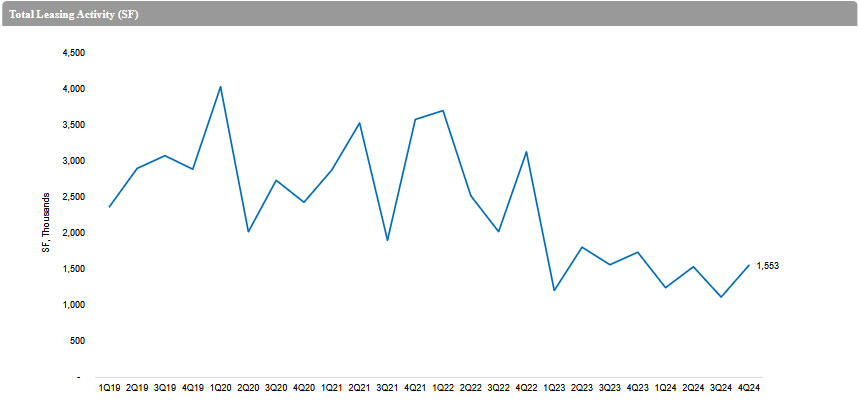

- Leasing volume reached approximately 1.9 million square feet, a slight dip from Q1 but consistent with seasonal patterns.

- Third-party logistics (3PLs) and retail distributors remained dominant, accounting for over 60% of new leases.

- Notable deals included Amazon, FedEx, and Costco, each securing space in the I-880 Corridor and Richmond submarkets.

Vacancy & Availability

- Overall vacancy rose modestly to 5.3%, driven by speculative deliveries and tenant relocations.

- Class A product in core submarkets like Hayward and Fremont continues to outperform, with vacancy rates below 3%.

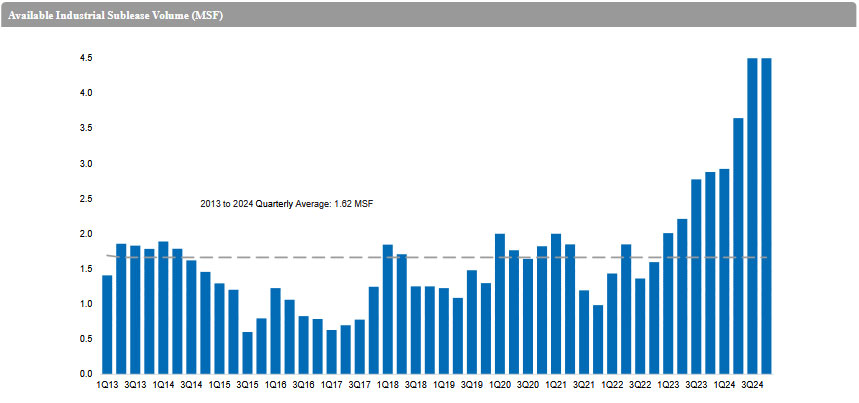

- Sublease space increased to 1.2 million square feet, signaling cautious optimism among tenants adjusting footprints.

Rents & Investment Activity

- Asking rents held firm at $1.45 per square foot/month, reflecting landlord confidence and limited new supply.

- Investment sales slowed slightly, with cap rates stabilizing around 5.1%. Institutional buyers remain active, especially for infill assets with strong transportation access.

Development Pipeline

- 2.8 million square feet of industrial space is under construction, with major projects in Oakland Airport and Union City.

- Developers are prioritizing ESG-compliant designs, including solar integration and EV infrastructure, to meet tenant sustainability goals.

Outlook

Despite macroeconomic uncertainty, East Bay/Oakland’s industrial market remains a magnet for logistics, e-commerce, and retail distribution. With strategic location advantages and a robust tenant base, the region is well-positioned for long-term growth.